Healthcare and Budget on the Road for Retirees

Retiring into vanlife or full-time RV travel is an incredible way to enjoy freedom, flexibility, and a simpler lifestyle. But even when your home has wheels, one thing doesn’t change: you still need a clear plan for healthcare and your overall retirement budget. For U.S.-based retirees aged 65+, healthcare is one of the most significant and predictable expenses, and understanding how it fits into a mobile lifestyle is essential if you want to travel with confidence.

This guide is based on national spending patterns for retirees aged 65+ and adapts them to the realities of nomadic living. It explains how much retirees typically spend on healthcare, how those costs fit into the total retirement budget, and what vanlife travelers can do to plan smarter coverage and spending while on the road.

Key takeaways: Healthcare and budget on the road

- Healthcare typically accounts for roughly 13–16% of the total budget for households aged 65+.

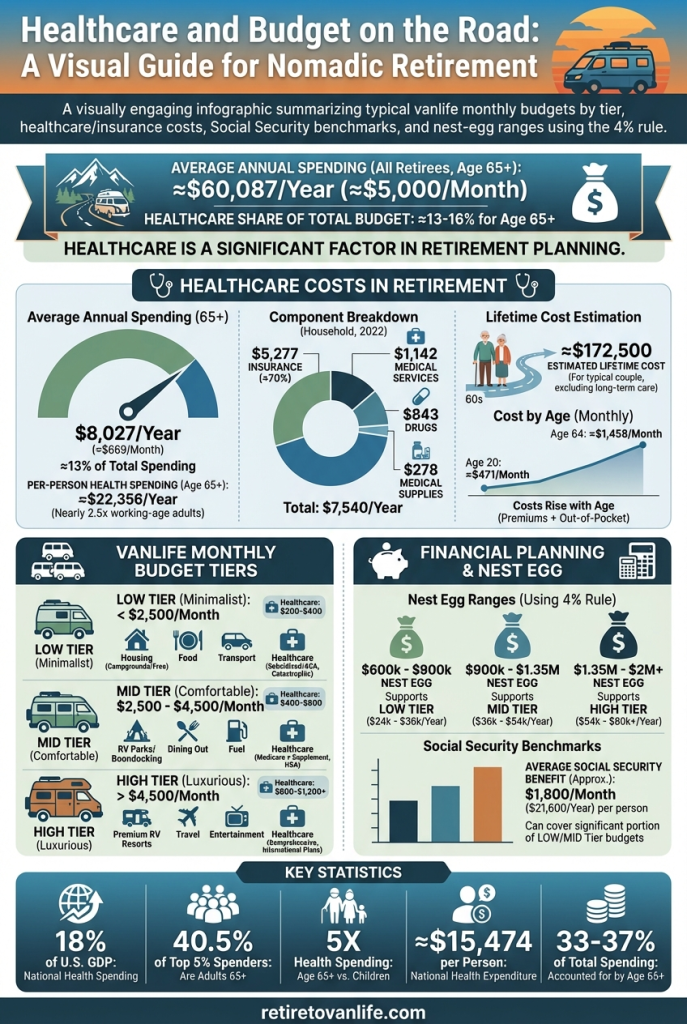

- Average total spending for 65+ retirees is around $60,087 per year (about $5,000 per month) in 2023.

- Average annual healthcare spending for age 65+ is about $8,027 per year (≈$669 per month), about 13% of total spending.

- Detailed breakdown (2022): Total ≈ $7,540 per year; $5,277 health insurance; $1,142 medical services; $843 drugs; $278 medical supplies.

- Per-person health spending, age 65+ (all payers) in 2020 was ≈ $22,356; adults 65+ are 17% of the population but account for ~37% of all health spending.

- National health expenditure per person (all ages) is ≈ $15,474 in 2024; health spending is ~18% of U.S. GDP.

- Average retiree healthcare share of total retirement spending (for people in their 60s) is ≈ 13%.

Why healthcare planning matters for nomadic retirement

When you retire into vanlife, you trade a fixed address for flexibility, but your body still has its own schedule, needs, and vulnerabilities. Healthcare is one of the few categories that tends to increase with age, no matter how minimal your lifestyle becomes. For nomadic retirees, the challenge is not just paying for healthcare, but making sure your coverage and access still work when you’re constantly changing locations.

You’re balancing two realities:

- Predictable costs like Medicare premiums, Medigap or Medicare Advantage plans, and regular prescriptions.

- Unpredictable needs like urgent care visits, specialist appointments, or hospital stays in unfamiliar towns.

Because healthcare typically represents around 13–16% of a retiree’s total budget, it’s a category that deserves deliberate planning—especially when your lifestyle is built around movement, not staying put.

National spending patterns for retirees aged 65+

Looking at national averages gives you a benchmark. You may spend more or less depending on your health, location choices, and insurance decisions, but these numbers provide a solid starting point for planning vanlife on a realistic budget.

Average total spending for retirees

Households aged 65+ spend about $60,087 per year, or roughly $5,000 per month. That total includes:

- Housing (rent, mortgage, property taxes, or campground fees and RV costs)

- Food and groceries

- Transportation (fuel, maintenance, insurance)

- Healthcare

- Entertainment and travel

- Miscellaneous expenses

For vanlife retirees, housing costs may drop compared to a traditional home, but fuel, maintenance, and campground or park fees can rise. Healthcare, however, tends to remain a stable and significant slice of the pie.

Average annual healthcare spending

On average, retirees aged 65+ spend about $8,027 per year on healthcare, or roughly $669 per month. That’s about 13% of total spending, which lines up with long-term national trends.

For a nomadic retiree, this means that even if you optimize other categories—downsizing, boondocking, cooking in the van—healthcare will still demand a meaningful share of your budget.

Detailed healthcare breakdown

A more detailed look at healthcare spending for retirees shows where the money actually goes. In 2022, the average annual healthcare spending of about $7,540 broke down roughly as:

- $5,277 – Health insurance: Medicare Part B, Part D, Medigap, or Medicare Advantage premiums.

- $1,142 – Medical services: doctor visits, outpatient care, tests, and procedures.

- $843 – Prescription drugs: ongoing medications and short-term prescriptions.

- $278 – Medical supplies: over-the-counter items, equipment, and other health-related products.

For vanlife retirees, these categories still apply—you’re just managing them while moving between states, regions, and healthcare networks.

The bigger picture: National health expenditures

Healthcare isn’t just a personal budget line; it’s a major part of the U.S. economy. Adults aged 65+ are a relatively small share of the population but account for a large share of total health spending.

- Per-person health spending for adults 65+: about $22,356 per year (all payers).

- Population share: adults 65+ are about 17% of the population but account for roughly 37% of all health spending.

- National health expenditure per person (all ages): about $15,474.

- Share of GDP: healthcare accounts for around 18% of U.S. GDP.

For someone planning to retire to vanlife, these numbers are a reminder: healthcare costs are not going away. The goal isn’t to avoid them, but to plan for them in a way that supports your freedom on the road.

How healthcare fits into a nomadic retirement budget

A mobile lifestyle changes many parts of your budget. You might spend less on traditional housing and more on fuel and maintenance. But healthcare tends to remain relatively stable and must be built into your long-term plan.

1. Insurance premiums

For most U.S. retirees, the largest healthcare expense is insurance. This usually includes:

- Medicare Part A and Part B (hospital and medical insurance)

- Medigap (supplemental) or Medicare Advantage plans

- Medicare Part D prescription drug coverage (if not included in an Advantage plan)

As a nomadic retiree, the key is choosing coverage that still works when you’re traveling across multiple states, not just in one local area.

2. Out-of-pocket costs

Even with good insurance, you’ll still have:

- Copays and coinsurance for doctor visits and treatments.

- Deductibles that must be met each year.

- Urgent care or emergency room costs when something happens on the road.

- Potential out-of-network charges if your plan has limited geographic coverage.

For vanlife retirees, out-of-network issues can be a real risk if you choose a plan with a narrow regional network.

3. Prescription costs

Prescription spending depends on your health conditions and the medications you take. As a nomad, you also have to think about logistics:

- Using national pharmacy chains so you can refill in different states.

- Mail-order prescriptions and how they work with mail forwarding or a home base address.

- Planning ahead so you don’t run out of medication in remote areas.

4. Preventive and routine care

Preventive care—checkups, screenings, vaccinations, and routine lab work—is essential for staying healthy on the road. It’s easier to handle small issues early than to deal with emergencies in unfamiliar places.

Many nomadic retirees schedule their annual or semi-annual appointments in specific “hub” cities where they return regularly, then travel more freely in between.

Healthcare challenges unique to nomadic retirees

Living on the road introduces challenges that traditional retirees don’t face. Understanding these ahead of time helps you design a healthcare strategy that supports your lifestyle instead of limiting it.

1. Network limitations and plan choice

Some Medicare Advantage plans are built around local networks. They may work well if you stay in one city or region, but can be restrictive if you’re constantly moving. Many nomads prefer:

- Original Medicare plus a Medigap plan for broad nationwide acceptance.

- Medicare Advantage PPO plans with wider networks and out-of-network options.

The right choice depends on your health, budget, and how widely you plan to travel.

2. Access to care in remote areas

Rural and remote areas can have fewer doctors, fewer specialists, and longer wait times. If you love boondocking or staying off-grid, you’ll want to think about:

- How far you are from the nearest urgent care or hospital.

- Whether you have a plan for emergencies.

- How quickly you can relocate if you need care.

3. Prescription logistics on the road

Managing prescriptions while traveling full-time requires a bit of strategy:

- Align refills so you can pick them up at predictable intervals.

- Use chains or mail-order services that work across multiple states.

- Keep a small buffer supply (where allowed) so delays don’t leave you without medication.

4. Emergency preparedness

Nomadic retirees should think through what happens if a serious medical event occurs far from their usual providers. That might include:

- Understanding how your insurance handles emergency care in other states.

- Considering travel insurance or emergency medical evacuation coverage for certain trips.

- Keeping key medical information and documents easily accessible in your van or RV.

Budgeting strategies for healthcare on the road

You can’t control everything about healthcare costs, but you can build a budget and system that makes them more predictable and less stressful.

1. Create a dedicated healthcare fund

One practical approach is to set aside a separate healthcare fund, ideally covering at least 12 months of expected healthcare expenses. For many retirees, that means saving somewhere in the range of $7,500–$9,000 as a dedicated buffer.

Keeping this money in a liquid account (like a high-yield savings account) gives you flexibility for premiums, prescriptions, and unexpected bills.

2. Choose insurance that supports mobility

When you retire to vanlife, your insurance needs to travel with you. Look for:

- Nationwide networks or broad provider acceptance.

- Telehealth coverage so you can handle minor issues from your campsite.

- Flexible prescription options that work across multiple states.

It’s worth taking the time to compare plans with a focus on how they work for travelers, not just for people staying in one ZIP code.

3. Use telemedicine whenever possible

Telehealth has become a powerful tool for retirees on the road. It can:

- Reduce the need to drive long distances for minor issues.

- Help you avoid out-of-network clinics for simple concerns.

- Provide continuity with a familiar provider even when you’re in a different state.

4. Plan your route around healthcare needs

If you have chronic conditions or regular specialist appointments, you can build your travel calendar around them. For example:

- Return to a “home base” city once or twice a year for checkups and tests.

- Stay longer in areas with strong medical infrastructure when you know you’ll need care.

- Use quieter travel periods for routine appointments.

5. Track your healthcare spending monthly

Healthcare costs can fluctuate, especially with unexpected visits or new prescriptions. Tracking your spending month by month helps you:

- Spot trends early (rising prescription costs, frequent copays, etc.).

- Adjust your budget before small changes become big problems.

- Make more informed decisions about where to cut or where to add buffer.

How much should nomadic retirees budget for healthcare?

Based on national averages, a realistic annual healthcare budget for a nomadic retiree is in the range of $7,500–$9,000 per year, or about $625–$750 per month. This aligns with:

- Average retiree healthcare spending.

- Typical Medicare premiums and supplemental coverage.

- Expected out-of-pocket costs and prescriptions.

If you have chronic conditions, multiple medications, or prefer more comprehensive coverage, you may want to budget above this range. The key is to be honest about your health and build a plan that supports your real needs, not just the ideal scenario.

Frequently asked questions about healthcare and vanlife retirement

Is vanlife realistic for retirees with health issues?

Yes, many retirees with health conditions successfully live on the road. The difference is that they plan more carefully around access to care, prescription logistics, and insurance coverage. You may need to travel more slowly, stay closer to larger towns or cities, and schedule regular check-ins with your providers—but vanlife can still be very doable.

Should I keep a home base for healthcare?

Some retirees choose to maintain a home base or use a mail-forwarding address in a state that works well for both taxes and healthcare. A home base can make it easier to:

- Maintain relationships with primary care providers.

- Schedule annual appointments in one familiar location.

- Handle mail, prescriptions, and legal documents.

Others go fully nomadic and rely on nationwide networks and telehealth. Both approaches can work—it depends on your comfort level and health needs.

What happens if I need emergency care far from home?

In a true emergency, you’ll be treated at the nearest appropriate facility. After that, your insurance coverage and out-of-pocket costs will depend on your plan. This is why it’s important to:

- Understand how your plan handles out-of-area emergencies.

- Carry your insurance cards and a summary of your medical history.

- Have a plan for follow-up care once you’re stable.

Can vanlife help me save money overall, even with healthcare costs?

For many retirees, yes. By reducing or eliminating traditional housing costs, you can free up money for travel, experiences, and healthcare. The key is to be realistic about fuel, maintenance, campground fees, and insurance—then layer healthcare on top as a non-negotiable part of the budget.

Final thoughts: Healthcare confidence for life on the road

Retiring to vanlife is about more than chasing sunsets and scenic campsites—it’s about designing a lifestyle that supports your freedom, health, and peace of mind. Healthcare will always be a major part of that equation, especially for retirees aged 65 and over.

By understanding national spending patterns, planning for insurance and out-of-pocket costs, and building a flexible healthcare strategy, you can travel with confidence. You don’t have to choose between adventure and security. With a thoughtful budget and the right coverage, you can have both: a life on the road and a healthcare plan that keeps you rolling.

On Retire to Vanlife, healthcare is just one pillar of a bigger picture—alongside budgeting, safety, community, and choosing the right rig. When you treat healthcare as a core part of your vanlife plan, not an afterthought, you give yourself the best chance to enjoy the journey for years to come.

As an affiliate, I earn from qualifying purchases at no extra cost to you.

As an affiliate, I earn from qualifying purchases at no extra cost to you.